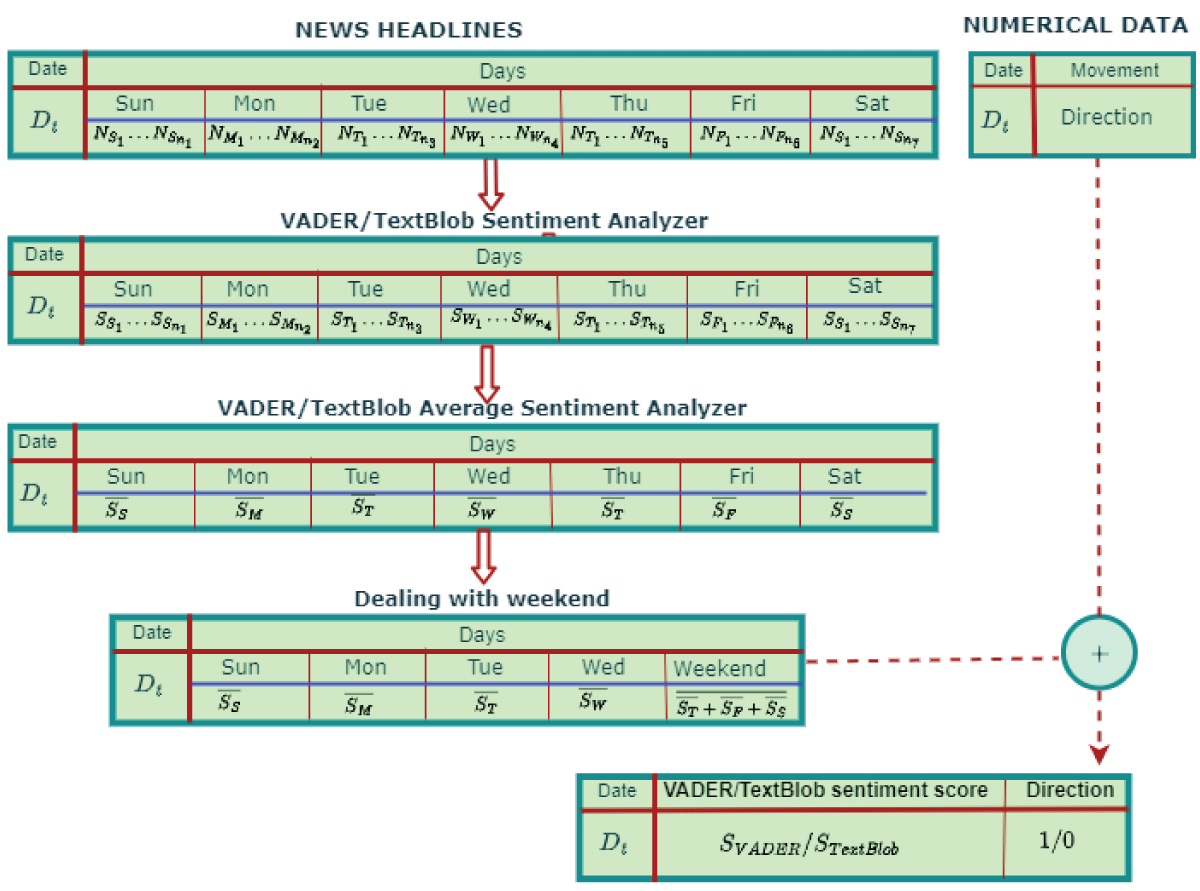

要約

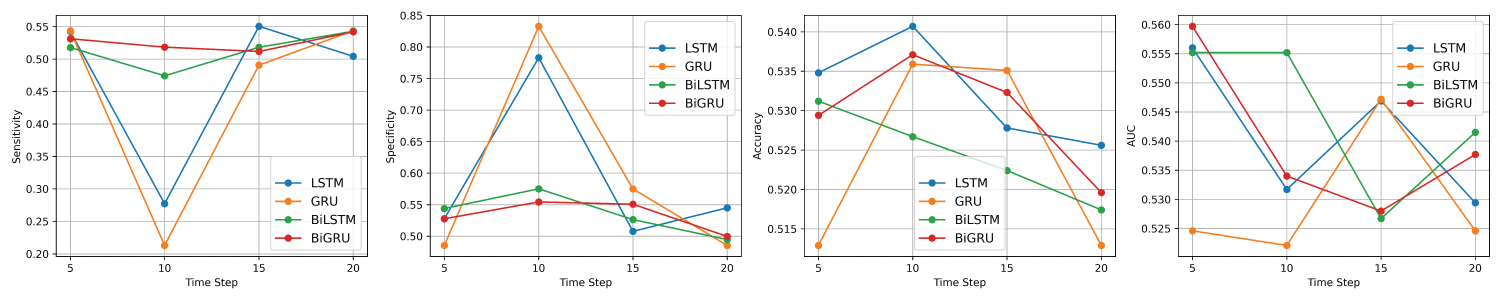

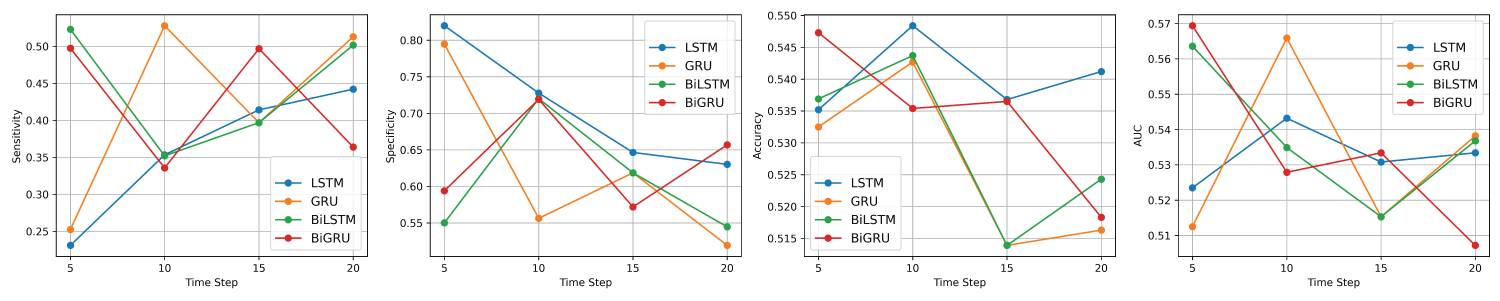

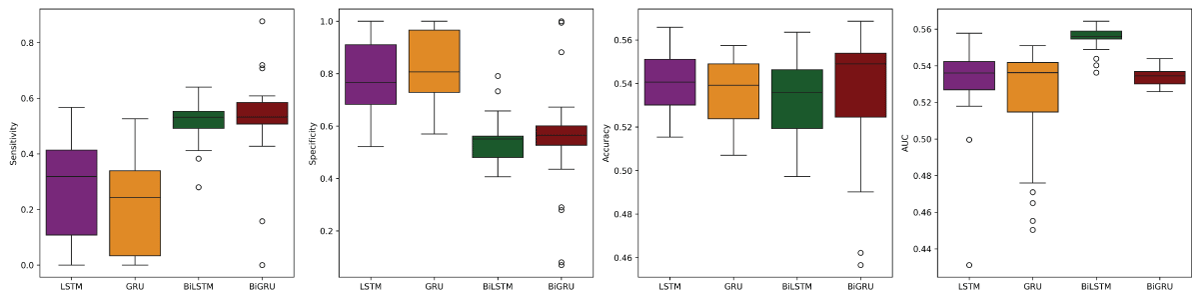

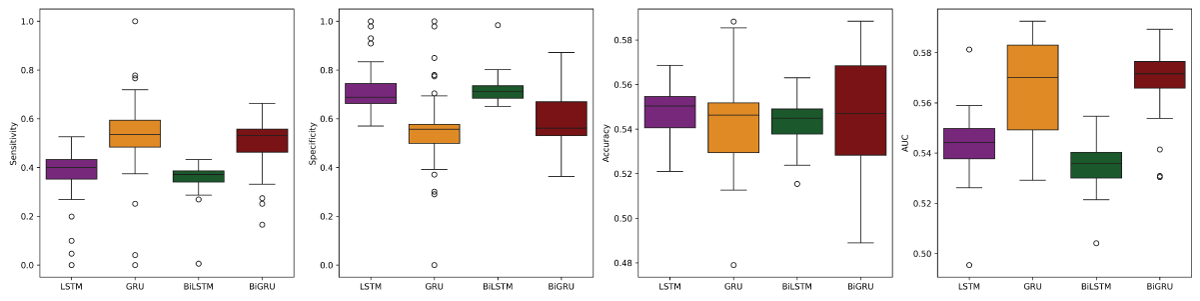

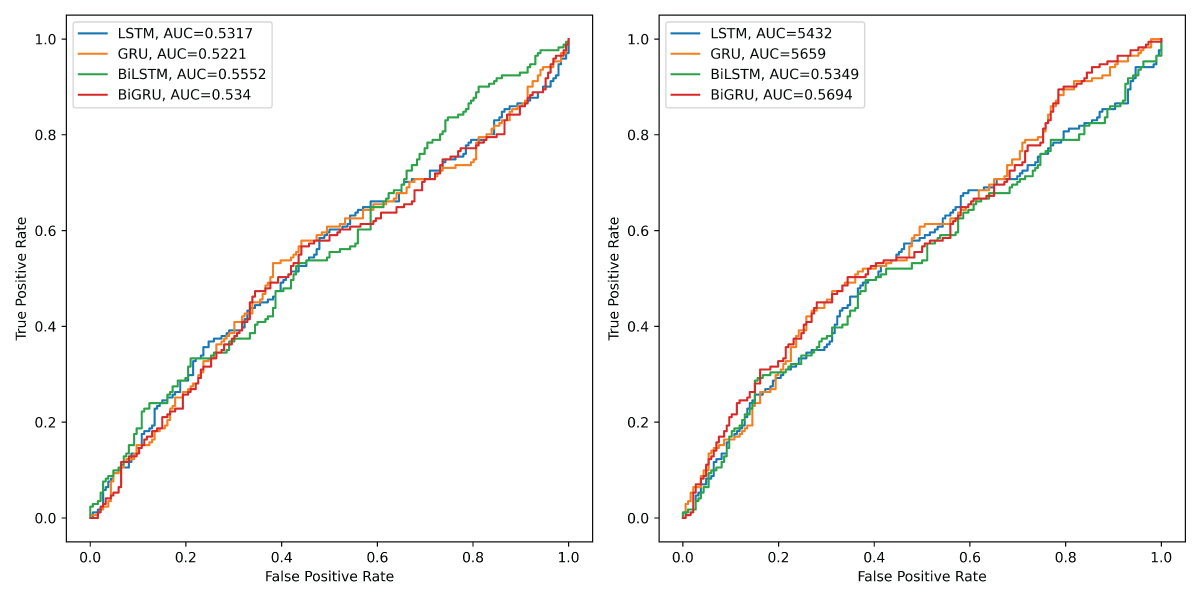

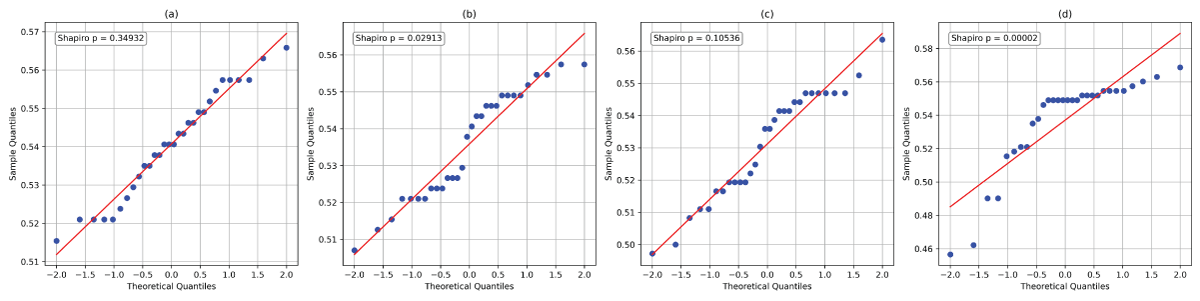

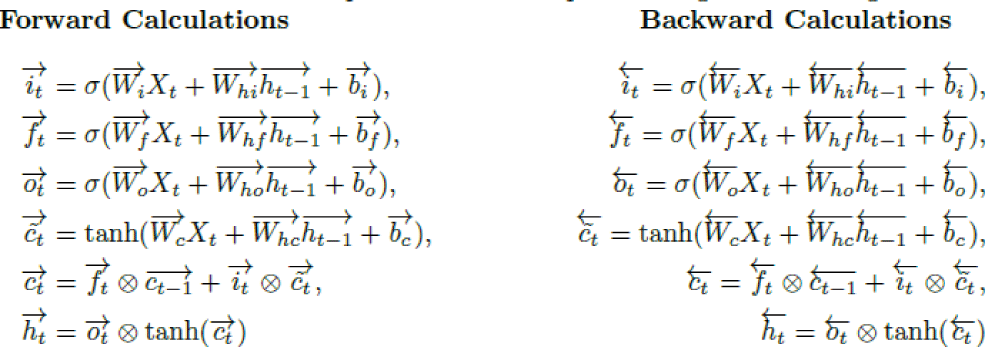

Predicting the direction of stock market movements is a challenging task due to its fuzzy, chaotic, volatile, nonlinear, and complex nature. However, with advancements in artificial intelligence, abundant data availability, and improved computational capabilities, creating robust models capable of accurately predicting stock market movement is now feasible. This study aims to develop a predictive model using news headlines to forecast the direction of stock market movements. It conducts a comparative analysis of four supervised classification deep learning models —long short-term memory (LSTM), gated recurrent unit (GRU), bidirectional long short-term memory (BiLSTM), and bidirectional gated recurrent unit (BiGRU)—to predict the next day’s movement direction of the close price of the Nepal Stock Exchange (NEPSE) index. Sentiment scores from the news headlines are computed using the Valence Aware Dictionary for Sentiment Reasoning (VADER) and the TextBlob sentiment analyzer. The models’ performance is evaluated based on sensitivity, specificity, accuracy, and the area under the receiver operating characteristic (ROC) curve (AUC). Experimental results indicate that all four models perform similarly when using sentiment scores from either VADER or TextBlob. Additionally, GRU and BiGRU models show consistent performance across both sentiment analyzers. However, LSTM and BiLSTM perform slightly better with TextBlob sentiment scores compared to those from VADER. These findings are further validated through statistical tests.